I recently reviewed the cost-of-living index at Cost of Living Index by State 2022 (worldpopulationreview.com). Here we can see the cost of living for each state in the United States. The cost-of-living index is calculated by determining a baseline for comparing costs across the United States. The cost-of-living index baseline is set at 100. States are measured against this baseline. By using this index, a state with a cost-of-living index of 400 is four times as expensive as the national average, and a state with an index of 200 will cost twice the national average. Currently, Florida is 100.3 which is right at the national average.

The cost of living is just half of our problem. The other part of our problem is some of us have a lot of debt. In the United States of America 42.9 million Americans have federal student loans. The total amount of student loan debt is $1.75 trillion in total. By age 24 or younger owe $110 billion, 25 to 34 owe $500 billion, 35 to 49 owe $622 billion, 50 to 61 owe $282 billion, and 62 and older owe $98 billion. Looking at these numbers, young professionals have over 990 billion in student loan debt, but it doesn’t stop there…

Americans have over $841 billion of credit card debt in 2022. According to Experian, between the ages of 20-29, there’s an average credit card debt between $1,881 and $3,927. For ages 30-39 the average credit card debt was $4,216 – $6,827. Some credit cards have high APR (Annual Percentage Rate. The annual Percentage Rate is the amount of interest paid back on the balance on the card annually. If we are carrying a balance and can’t and can only afford the minimum payment, the bank is making interest off of our balance, and…the balance is still owed, but it doesn’t stop there…

Although our debt is high some of us have not adjusted our spending habits so that we can address the debt that we owe. The Federal Reserve raised interest rates this year and the APR on credit cards will grow and the cost of carrying debt will worsen for some. Debt is an issue for us as young professionals and so I created Signify! Not to highlight ways we can address debt, but to share different ways we invest in ourselves and achieve financial independence. If you haven’t realized it by now the times are changing and we also need to be intentional about our well-being and those who come after us.

So, what’s my plan for paying down debt?

First I must take responsibility for the debt. There were some unnecessary costs that I took on and I will address the issue by creating a plan of action. This isn’t my first rodeo paying down credit card debt. It just wasn’t this much and back in 2017 inflation wasn’t something to take into consideration.

I created a debt balance sheet. On this balance sheet, I will track our debt starting with the debt that has the highest interest. For my household that is credit card debt.

Here is an example of what the debt balance sheet looks like. A balance sheet will help me keep up with the amounts I paid. Creditors typically don’t send multiple updates to the credit bureaus every time we make a payment.

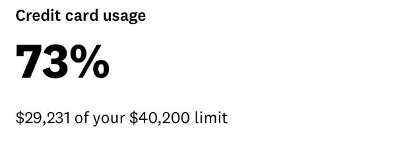

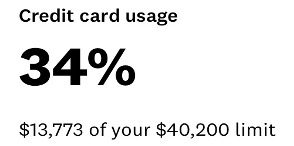

Debt Status as of June 2022

This is where we stand as of June 2022. We are currently $29,231 in credit card debt. So, some of you might be wondering how the heck did you do that. Well to sum it all up, we had no emergency fund, made poor decisions, and used both credit and debit at the same time, resulting in an inability to pay off the balances each month.

In 2022 our goal was to increase our income and cut back a lot. So, we rarely take trips, eat out, buy outside our budget, and limit Hobby Lobby and Target shopping (if you know…you know). We were able to increase our income enough to pay close to $5,000 a month towards our credit card debt. We will be paying our credit card debt from now until late November 2022. I’ve already had to break the news that we might not be leaving town this year for the holidays.

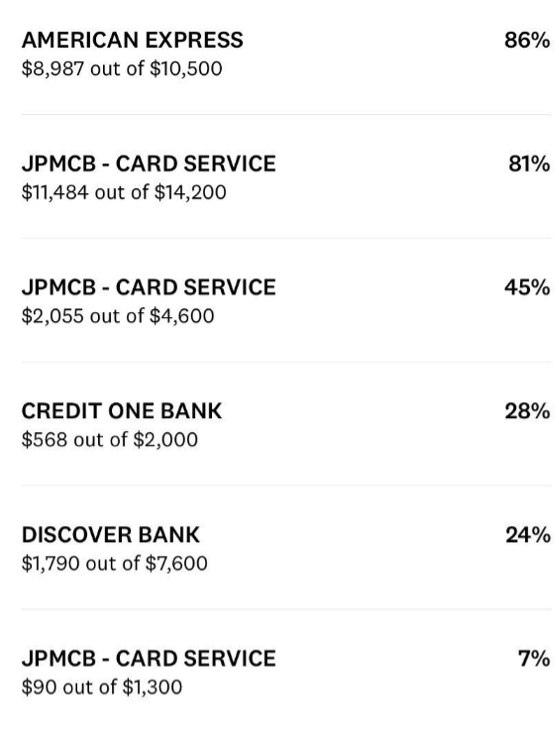

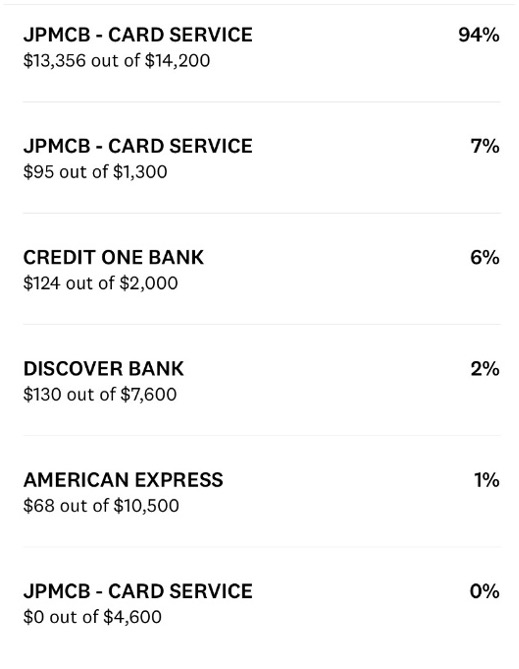

Most of our spending was done on the three cards listed below. I will tweak the snowball method and start paying off the discover card first and then I will move on to the Amex.

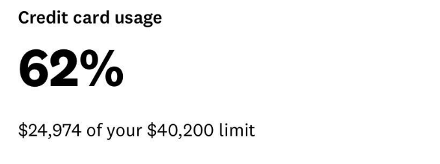

Debt Status as of July 2022

As of July 1st, this is where we stand. We are down to $24,974. This month the Federal Reserve is going to raise interest rates again to try to get inflation under control. So, I will monitor to see if the rates will rise by 50 basis points or 75 basis points. For those who haven’t heard of basis points before. A basis point is one-hundredth of a percentage point. For example, the difference between 1.75% and 1.85% is ten basis points. The Federal Reserve usually goes up or down 25 basis points. When the Fed raises interest rates credit card debt also rises. The APR on most cards increases unless your card is still offering 0% APR.

If the Fed continues to be aggressive, I might also consider paying down balances more aggressively. The minimum payment for the Amex card is $288 per month and the Chase card is $358. If the fed raises interest rates those minimum payments will continue to grow. So, if the Fed does increase by 75 basis points, then I’ll have to head to the drawing board once again.

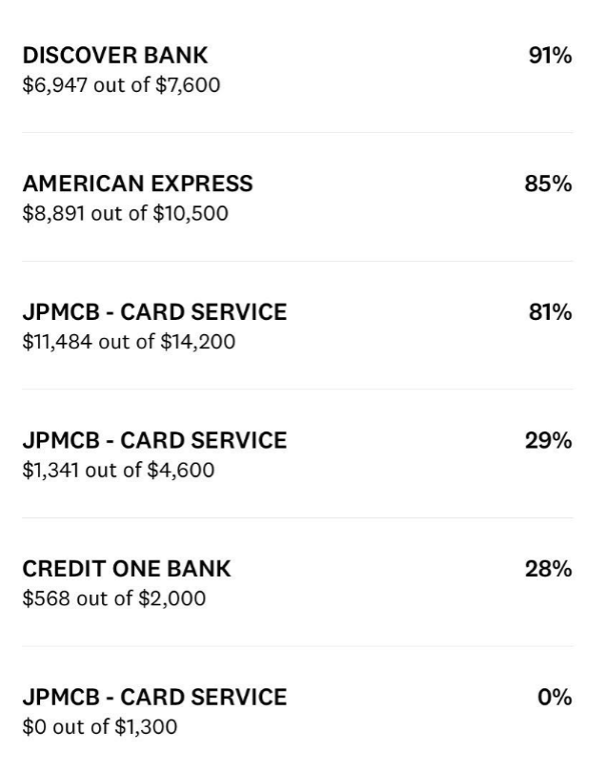

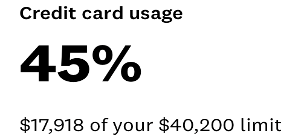

Debt Status as of August 2022

We’ve officially crossed a milestone and the amount owed is now under 50%. I celebrated for 5 minutes and got my game face back on. I understand that the job isn’t done and we have more work to do. Some of the cards have been used to take care of some needs. For example, the Credit One card had a few charges due to my dog getting an ear infection. Overall progress is being made and we are still on track to get everything paid down before the New Year.

The Fed did increase interest rates by 75 basis points. The charge that you see on the Amex card is the interest. This was posted right as we paid off the card. When we carried a balance, interest dropped on the total every month. So interest accrued about $194 per month. Well, no more of that after we pay off the balance! The goal for the next few weeks will be to work on cards 2-4. My goal is to pay the balances off so I can use what would have been the“minimum payments” to add to the amounts to pay off card 1. We are on pace to start paying down card 1 in mid-September.

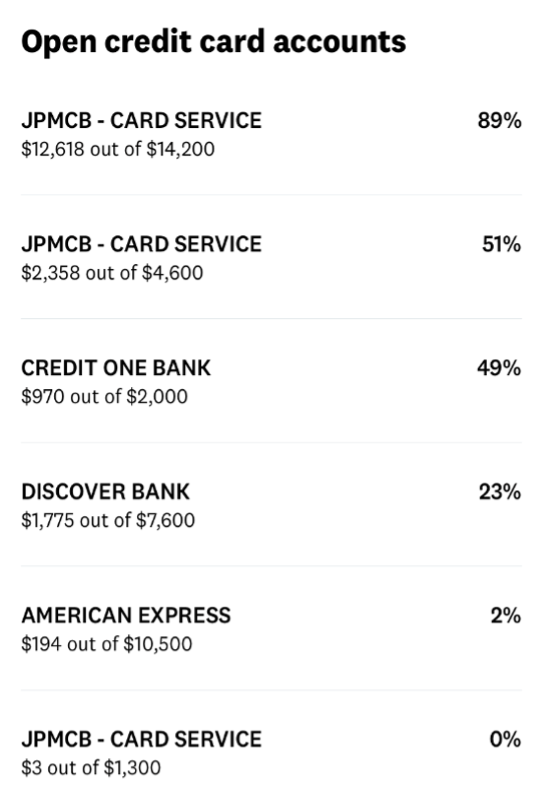

Debt Status as of September 2022

As of September, this is where we stand. Right now we are working on the Chase card at the top. This month we weren’t able to add as much as we used to. For the past couple of months, we’ve been cutting into groceries and having close to nothing in the account. It’s no longer sustainable as costs increased in utilities, food, etc. We’re on pace to finish paying off the credit cards around mid-December instead of late November. We made a payment on the Chase card but it hasn’t been reflected yet. We will share the update in October.

The Fed mentioned that it will continue to raise interest rates and I feel for those who are struggling with debt. Especially credit card debt. As I shared earlier on this journey, we were paying over $1000 a month on minimum payments. Not to mention the interest charges would eat into the amounts being used to pay down the balances. If you’re currently deep in credit card debt do not put it off to the side, create a plan and take action.

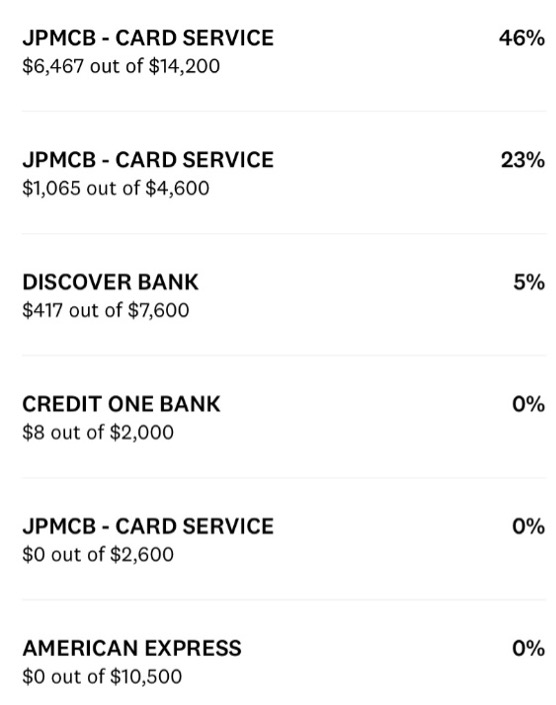

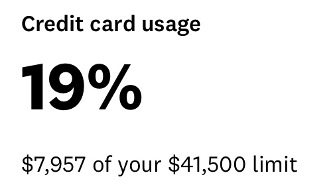

Debt Status as of November 2022

I was unable to take notes in October, so this is the progress for both October and November. We are finally down to 4 digits. After spending quite some time in the 5-figure range. I planned to finish paying off the cards by December however that will not be the case. We will get close but won’t finish the job until January 2023. So, it will be a little over 8 months. The bulk of the payments are due on the Chase card.

This month I saw the difference in the checking account. Not having to pay $726 in minimum payments due to the cards being paid down feels like the hard work is paying off. I also received a credit line increase on one of the cards. This helps credit utilization so I’m grateful for the increase. We still have a little way to go. The journey is not over but we have come a long way.

The Fed will continue to raise interest rates to cool off the economy. Fed chair Powell has shown that he is not bluffing. Most of the job cuts we see are in tech. The recession talks haven’t died down at all especially now that elections have happened. There are a few important job reports that will be coming out in December. If the economy remains hot the Fed will continue raising interest rates into 2023.