Credit Report Guide for Beginners

I stumbled on a very interesting post by the New York Post. The title was “Shocking percentage of Americans don’t know their credit score”. I began to read and was intrigued to learn why that was the case. According to the article “One in eight Americans are unaware of their credit score, according to new research. A study conducted by OnePoll in conjunction with LendingPoint examined the credit score knowledge and lending habits of respondents.” What was also alarming from this research was 71 percent of those studied are unaware of the various ramifications associated with a bad credit score. Also, 44 percent didn’t know that higher rates and more restrictive terms on any approved loans can accompany a poor credit score. Seven in 10 of those studied say they have personally felt held back in life because of a poor credit score.”

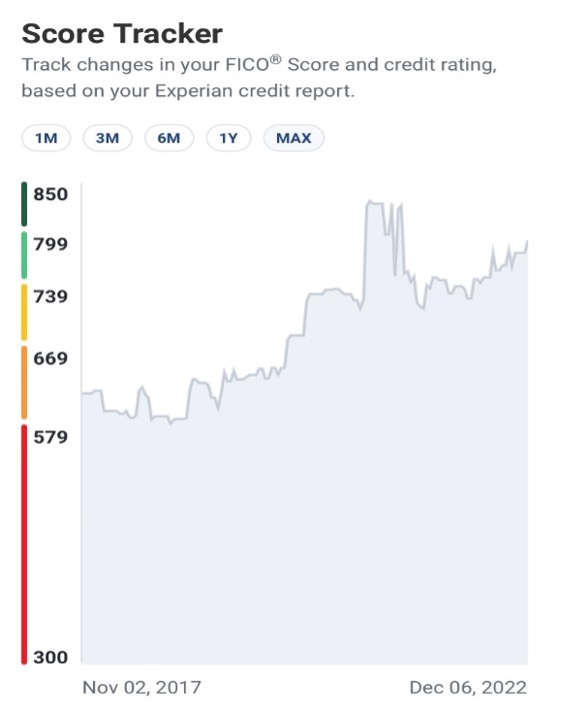

I’ve had my ups and downs with credit before. I recently paid down over $26,000 in credit card debt. Back in 2017, I had a credit score of 580. Now my credit score is over 750. I say this not to brag, but to give transparency that I had to make changes and work hard to get my score to where it is now.

The current economic climate has not been kind to us who carry debt. At one point I paid over $1000 on minimum payments each month. I had to get my act together and put what I learned about credit into practice. Building credit and fixing credit can be a journey but fixing our credit so that we can gain access to more capital and resources is something we should all be striving to do not just for us but for our families as well. In this eBook you will learn:

- What is credit, credit report, and different sections on our credit report, and what they mean

- What are credit scores and how does a credit score work?

- How can we work on our credit score and what can we do to boost our score

- Different types of credit cards and credit profiles

- No, No’s of building credit

- How to apply for credit and how can we leverage our good credit

- How to deal with collections and student loan debt

- How to protect yourself from identity theft

- Credit laws and Consumer Rights Protection

- Important Credit Terms

Chapter 1

What is credit, credit report, and different sections on our credit report?

What is credit?

Credit is a key concept in personal finance. It refers to the ability to borrow money from financial institutions, usually in the form of a loan. The creditworthiness of an individual or entity is determined by credit history, which is a record of past borrowing and repayment activity. A good credit history indicates that an individual or entity is a responsible borrower and is more likely to repay their debts on time. A bad credit history, on the other hand, may make it difficult to obtain a loan or may result in higher interest rates.

What is a credit report?

A credit report compiles the credit history of an individual. The information is housed mainly within three credit bureaus and contains the individual’s history of borrowing, payment timeliness, and the number of credit inquiries.

Credit reports sum up how good we are at paying back debt. The lenders review our credit report to determine the risk in extending credit to us and what the lending terms will be. Names of the credit bureaus include Experian, Equifax, and Transunion. There have been reports that other credit bureaus exist, but the list above are the main three. Depending on which bureau’s report you are reviewing, some information may appear differently on each page.

Credit Report Sections

The Payment History

The payment history section of a credit report shows you how current your accounts are. For each month on each loan or credit line you have opened in your name, the report will indicate any payments that were 30 days, 60 days, 90 days, 120 days, 150 days, or 180 days past due. The report will also indicate any foreclosure proceedings, repossessions, insurance claims, collections, charge-offs, closed accounts, or display No data for the time, etc. The late payments are recorded on the credit file when the individual misses paying at least the minimum payment by the deadline designated by the lender/creditor. If a payment goes between 150 – 180 days past due, most creditors will send the account to a collections company. The Collections Department will try to get the past due debt repaid and your credit score will drop by 25-120 points.

Accounts that may be considered negative

As stated above some of the most common things that report negatively on your credit reports are charge-offs, collections, and bankruptcies. This negative information can remain on your credit report for 7 years for missed payments and up to 10 years for Chapter 7, 11, or 12, bankruptcies. If you have any potentially negative information on your credit report it will be listed under this section.

Credit Items/Account Details

Under this tab, you will see all accounts associated with your name and social security number listed. Here you will see the name of the creditor that lent you the line of credit or loan, your partial account number, and the creditor’s address and phone number.

There will be a few sections under this tab that provide details about the account. This includes:

- Date Opened– The date the account was opened.

- Address ID– The ID number that the credit bureau assigns to the address the creditor has on file for you.

- Type– Describes the type of account (i.e., credit card, mortgage, education (i.e., student loans), etc.

- Responsibility– This section specifies the ownership of the account (i.e., Individual, authorized user, or if the account is joint with someone else), etc.

- First Reported– The month and year the credit bureaus began reporting the account.

- Monthly Payment– The amount that is due to be paid monthly.

- Credit Limit– The line of credit that was approved and given to the account holder.

- High Balance– The highest balance that was carried on the credit card within a certain amount of time.

- Recent Balance– the previously reported balance on your credit line.

- Status– Shows the current status of the account (i.e., Open/never late, paid/closed, closed, etc.)

- Date of Status– The last time the status of the account was reported by the creditor to the bureau.

Credit Report Sections continued…

Account History

This section may show some of the following acronyms, (AB), (DPR),(SPA),(AAP), which stand for, the Account Balance, Date the payment was received, Scheduled Payments, and Actual Amount paid, respectively. This section will break down your balances owed from month to month. If you are carrying a balance, you will see the number of months that you have carried a balance and the amount owed each month. At the bottom of the account history, you will see the range of months you have carried a balance on the line of credit. For example, it may say “Between January 2019 and March 2020 your credit limit/high limit was $234.”

Credit Utilization

Credit Utilization is a percentage calculated from the total amount of credit currently used divided by the total amount of revolving credit you have. The rule of thumb is to try and keep your credit utilization under 20% for credit cards. For more diverse credit reports that include mortgages and real estate please speak to your financial advisors to understand your credit utilization percentage.

Credit Applications/ Hard Inquiries

Hard inquiries are requests that allow lenders to look at your credit report to see if they will be able to lend you a line of credit and on what interest rate terms. Be mindful of the number of hard inquiries you allow. Hard inquiries stay on your credit report for 2 years and can negatively impact your credit score.

Consumer Report Views/ Soft Inquiries

Soft inquiries are sometimes initiated by lenders or service providers to see if you pre-qualify instead of initiating a hard inquiry. Certain credit monitoring sites and software may use soft inquiries to update you on your credit score monthly, such as Credit Sesame or credit card company. Soft inquiries do not affect your credit score.

Personal information

This section shows the name and name variations reported on the credit bureaus’ database for an individual. For example, if your name is Brian John Henry, you may see variations such as Brian J. Henry or Brian Henry. It depends on the name variation you used when you applied for the line of credit. So be sure to check and review this section to make sure your name is being reported accurately. Also, there’s a section that displays address(es). These are addresses where you previously lived or currently live that are being reported on the credit bureaus’ database. Credit reports may also include an information section on your year of birth, telephone numbers, or current employers.

Chapter 2

What are credit scores and how does a credit score work?

What are credit scores?

Credit scores are numbers that creditors use to evaluate an individual’s creditworthiness. Scores range from 300 to 850, with higher numbers indicating more favorable credit risk.

CREDIT SCORE RANGES

FICO SCORE

- Exceptional 850-800

- Very Good 799-740

- Good 739-670

- Fair 669-580

- Very Poor 579-300

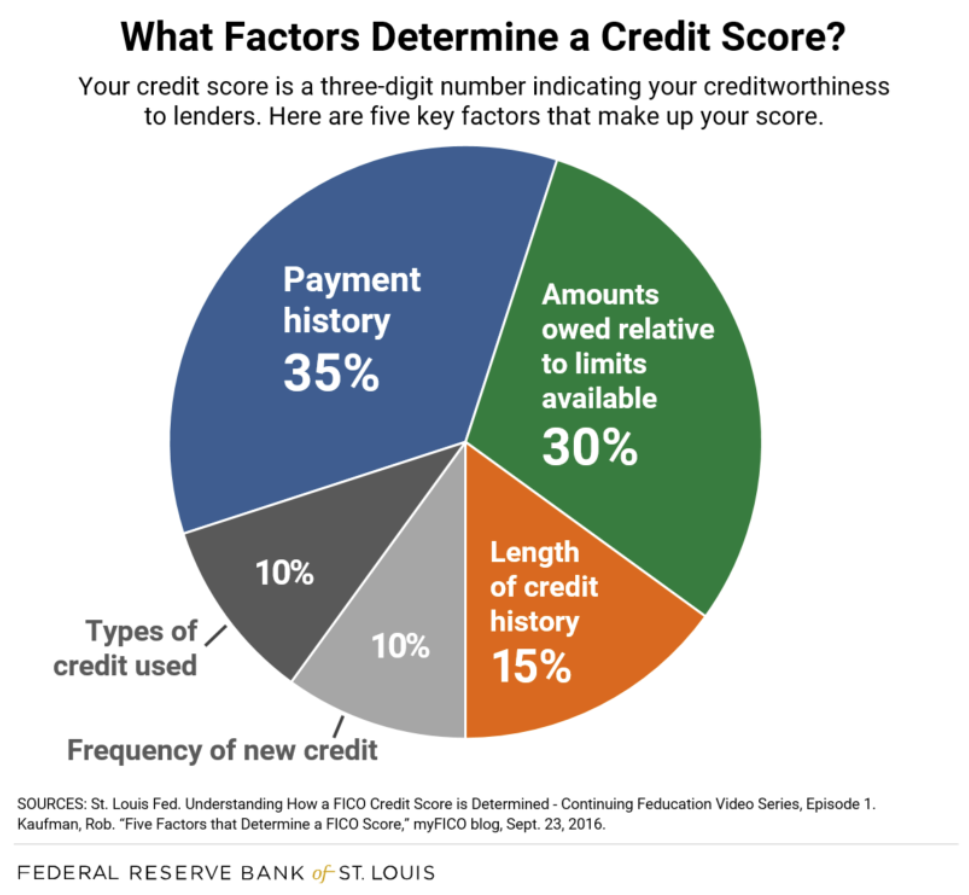

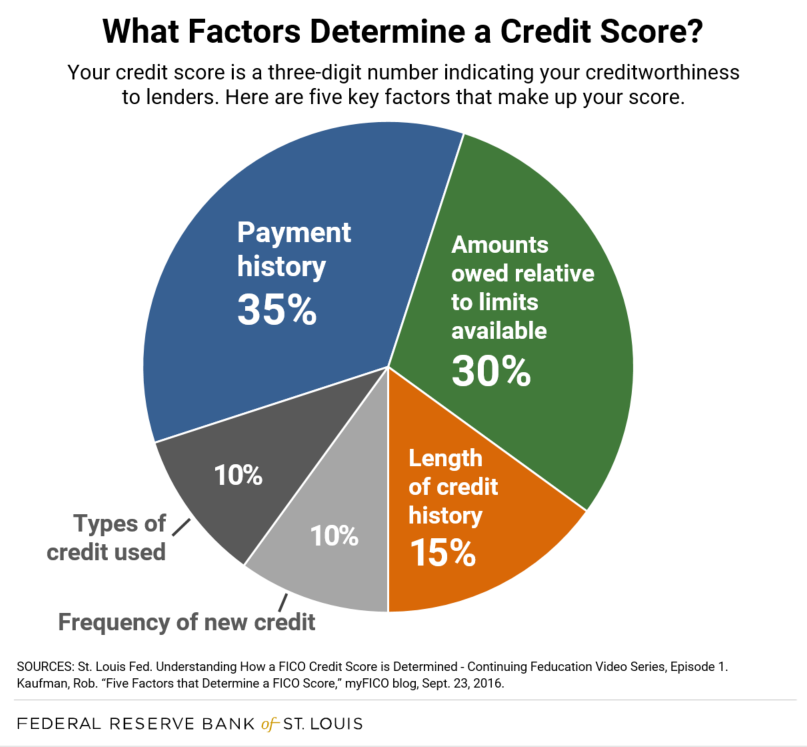

What determines our credit score?

Several factors go into determining your credit score, including:

- Payment history: Do you have a history of making late payments? This can hurt your score.

- Credit utilization: This is the amount of credit you’re using compared to the total amount of credit available to you. A high credit utilization ratio can hurt your score.

- Length of credit history: A long credit history can be beneficial to your score.

- Types of credit: Having a mix of different types of credit can be helpful to your score.

- Credit inquiries: too many credit inquiries can hurt your score.

Payment History

Payment history refers to the record of on-time or late payments that is reported to the credit bureaus by your creditors. Payment history makes up 35% of a FICO score, so it is one of the most important factors in determining your creditworthiness. A strong payment history shows creditors that you are responsible and likely to repay your debts. Conversely, a history of late payments can make it difficult to qualify for new credit.

Credit Utilization

Credit utilization is the amount of credit you have used in comparison to the amount of credit you have available. Credit utilization is often seen as an important factor in credit scoring models, and a high credit utilization ratio can indicate to lenders that you may be a higher-risk borrower. Credit Utilization accounts for 30% of your credit score.

There are a few different ways to calculate credit utilization, but a common method is to take your total outstanding credit balances and divide them by your total available credit. For example, if you have $1,000 in outstanding credit card balances and your total available credit is $5,000, your credit utilization ratio would be 20%. You can often improve your credit score by paying down your outstanding balances and lowering your credit utilization ratio.

Length of History

The length of credit history is the amount of time that you have had credit accounts open. It is one of the factors that lenders look at when considering a loan or credit application, and it can impact your credit score. A longer credit history shows that you have a good track record of managing credit and making payments on time, which can make you a more attractive borrower. If you have a shorter credit history, you may still be able to get approved for credit, but you may pay a higher interest rate. Your length of history is 15% of your credit score.

Types of Credit a.k.a Credit Mix

Credit mix is the variety of credit types (installment, revolving, etc.) that you have on your credit report. Lenders like to see a good mix because it shows that you’re able to handle different types of debt responsibly. A good credit mix can also help improve your credit score. Having a variety of credit types can help show lenders that you’re a responsible borrower. It can also help improve your credit score. So, if you’re looking to improve your credit, consider diversifying your credit mix. Credit Mix accounts for 10% of your credit score.

Here are some examples of different types of credit:

- Installment loans: These loans typically come with fixed payments and terms. Examples include student loans, auto loans, and personal loans.

- Revolving credit: This type of credit typically has no fixed payments or terms. Credit cards are the most common type of revolving credit.

- Mortgage loans: These loans are used to finance a home purchase. Mortgage loans typically come with fixed payments and terms.

- Lines of credit: These are similar to revolving credit, but they typically have a fixed limit. Home equity lines of credit are one type of line of credit.

Credit Inquiries

Credit inquiries are a record of who has accessed your credit report. Credit inquiries can be either soft inquiries or hard inquiries. Soft inquiries occur when you check your credit report or when a company checks your credit report for informational purposes. Hard inquiries occur when you apply for new credit and a lender accesses your credit report. Credit inquiries can stay on your credit report for up to two years, but they typically only affect your credit score for the first year. Credit inquiries account for 10 % of your credit score.

{kind=link}

Chapter 3

How can we work on our credit score and what can we do to boost our score?

Step 1. Get a copy of your credit report.

Download your Annual Credit Report- One way to monitor your score for free is to order your free annual credit report. You can receive your free online credit score by going to www.AnnualCreditReport.com. Click on “request your free credit score” and the website will prompt you to type in your personal information and ask you a few questions to confirm your identity. You are only able to get one free credit report a year. Due to the pandemic, you can get free credit monitoring more than once, but this feature may end at some point. You can access your credit report from this website as well as from the actual credit bureau websites.

*Side note- Please use a protected browser when accessing your credit report!

What are some ways we can monitor our credit for free?

Some banks provide your free FICO credit scores- Some banks provide your free FICO scores on your online banking app and website as a perk of being their customer. Most banks that offer this benefit will share your FICO score and it’s usually the score from Transunion and Experian. Normally, they don’t provide too many details or breakdowns of your score or credit history. It’s just an FYI on your score, but it is a free way to monitor your credit score at least.

Credit Karma– Credit Karma is an app that I’ve used for years to help keep up with my credit history information. I used to pay for credit monitoring with each credit bureau, but I felt that it was a waste of money when there were ways I could get credit monitoring for free. Credit Karma uses the Vantage score system which ranges from Exceptional 750-850, Very good 700-749, Good 650-699, fair 550-649, to poor 549-300. www.creditkarma.com

*Side Note– Your Vantage score is not the same as your FICO score. Lenders use the FICO score to determine your loan eligibility. The FICO and Vantage scoring systems have slightly different score ranges. For example, you can have a Vantage credit score that is considered exceptional, whereas that same score would be considered only very good under the FICO scoring system.

Credit Sesame– Credit Sesame is my favorite free credit monitoring app. I use their platform more than credit karma. Credit Sesame offers a lot more information about your credit score. If you are looking for an app to monitor your credit that provides breakdowns and explanations about what things mean, Credit Sesame is an AWESOME app for that! www.creditsesame.com

*Side note– Credit Sesame is powered by Transunion. Credit Karma gives you both TransUnion and Equifax credit information but does not have the extra information that Credit Sesame has to offer.

Experian- Experian is a great way to monitor your Experian credit report. You can get all three bureaus, but you will have to pay for that separately, unfortunately. The thing I like about Experian is that they provide your FICO score vs. the Vantage score which Credit Sesame and Credit Karma provide. www.experian.com

Credit Wise by Capital One– Credit Wise by Capital One offers free credit monitoring as well. Their website does break down your credit report and helps you to understand your credit! I haven’t been using their platform, but you can give them a try and let me know what you think about Credit Wise. www.creditwise.com/captialone

Step 2 Check for Inaccurate information and what is being reported as a negative item

Once you have your reports, go through them carefully and look for anything that doesn’t seem right. If you see something that looks incorrect, contact the credit reporting agency, and dispute the information. Keep in mind that it’s not always easy to spot inaccurate information on your credit report. If you’re not sure whether something is accurate or not, it’s always best to err on the side of caution and dispute it. That way, the credit reporting agency will have to investigate and determine whether the information is accurate or not.

Negative items on a credit report are negative entries that are made about your financial history. These negative items can include things like late payments, missed payments, or defaults on loans. Negative items can also include negative information that is reported by creditors, such as charge-offs or collection accounts.

Here are some additional examples of negative items:

- Late payments: This is when you make a payment after the due date. It will usually stay on your report for seven years.

- Charge-offs: This happens when you owe a creditor money, and they give up on trying to collect it from you. It will stay on your report for seven years.

- Collections: This is when you have unpaid debts that have been turned over to a collection agency. It will stay on your report for seven years.

- Foreclosures: This happens when you stop making payments on your mortgage and the lender repossesses your home. It will stay on your report for seven years.

- Bankruptcies: This is when you file for bankruptcy. It will stay on your report for 10 years.

If you find any information on your credit report that is old/ inaccurate correct those and update it on your credit profile. Some examples include the way that your name is spelled and, abbreviations of your name, for example, Chris Jones, Christ Jones, Christop Jones, when it should be Christopher. Also, check your date of birth to make sure that your birthday is reported correctly. For some items, you will have to send documentation to the credit bureaus proving that the information on file is incorrect. Documentation needed may include a driver’s license, state i.d, or birth certificate.

Step 3- Get caught up on your payments if you are behind.

Remember your payment history is one of the most important factors in your credit score. It accounts for over 35% of your credit score. Although you may not be able to change what’s already on your report, there are things you can do to improve your payment history going forward.

- – Make sure you pay all of your bills on time, every time. This includes credit cards, mortgages, car loans, and any other type of loan or bill you may have.

- – If you have trouble remembering to pay your bills on time, set up automatic payments from your bank account. That way, you’ll never miss a payment.

- – If you do miss a payment, make it a priority to catch up as soon as possible. The sooner you pay, the less damage it will do to your credit score.

- – If you’re having trouble making ends meet, contact your creditors, and see if you can work out a payment plan. Many creditors are willing to work with customers who are struggling to make their payments on time.

Step 4- Start paying down your credit card balances and create a plan to pay down debt.

Paying down debt is one of the best ways to start improving your credit score. Some may choose to get credit repair done and that is an option that is available to us all. However, if you can create a plan and pay down debt you should. Here are some tips on how to start paying down debt.

- Attack the debt with the highest interest rate first

This will save us money in the long run as we won’t be paying as much interest. When it comes to paying down credit card debt, many people focus on the debt with the highest balance. However, this may not be the best strategy if we want to pay off our debt as quickly as possible. Instead, attacking the debt with the highest interest rate first can help us get out of debt faster.

Here’s how it works: let’s say you have two credit cards, one with a balance of $1000 and an interest rate of 15%, and the other with a balance of $500 and an interest rate of 10%. If you focus on paying off the card with the higher interest rate first, you’ll save money in the long run. That’s because you’ll be paying less in interest charges overall.

- Negotiate with your creditors

Another strategy we may want to consider is negotiating with our creditors. By contacting our creditors and explaining our financial situation, we may be able to negotiate a lower interest rate or monthly payment. This can help us save money and pay off our debt faster. Of course, every creditor is different, and there’s no guarantee that we’ll be able to negotiate a lower interest rate. But it’s worth a try, especially if we’re struggling to make our monthly payments. If you’re not sure where to start, you can contact a credit counseling agency for help.

- Use a debt snowball

The debt snowball method is a popular way to pay down credit card debt. You start by paying off your smallest balance first and then move on to the next smallest balance. The idea is that by paying off your smaller debts first, you’ll get a psychological boost that will motivate you to keep going. There are a few different ways to calculate your debt snowball, but one popular method is to list your debts in order from smallest to largest, and then make payments on the smallest debt first while making minimum payments on your other debts.

- Use balance transfers or consolidate

Balance transfers can be a helpful tool in paying down credit card debt. By transferring your balance to a new card with 0% APR for a promotional period, you can save on interest and pay down your debt faster. By transferring your balance to a new card with a lower interest rate, you can save money on interest and pay off your debt faster. You can also consolidate your debt by taking out a consolidation loan. This will allow you to pay off all of your credit cards with one loan at a lower interest rate. Consolidating your debt means taking out a new loan to pay off multiple debts. This can help you save money on interest and fees, and it can also make it easier to manage your debt payments.

- Seek professional help

If you’re having trouble getting out of debt, seek professional help. A financial advisor can assist us in creating a budget and repaying our debt. There are a few different ways to get professional help with our credit card debt. We can work with a financial planner or counselor, or we can use a debt management plan. Working with a financial planner or counselor can help us develop a budget and come up with a plan to pay down our debt. This option may be best if we’re struggling to make ends meet and need help getting our finances in order.

We all have different credit profiles. Some of us have high credit card debt, but no student loan debt. Some might have no credit card debt and some student loans and medical debt owed. Some of us have a lot of debt in each category. Creating a plan is going to be central to your credit profile. If you need help with creating a more detailed plan, please reach out to a financial counselor.

How can we boost our credit score?

- Check your credit report regularly and dispute any errors you find.

- Make all of your payments on time, including credit card bills, utility bills, etc.

- Keep your credit utilization low by using only a small portion of your credit limit.

- If you have any old debts, try to pay them off as soon as possible.

- Apply for a secured credit card if you have bad credit or no credit history.

- Become an authorized user and add the history to your report. *make sure they have good credit and pay timely.

What can I do to improve my age history?

One way that we can add some credit history to our credit report is to find a family member or trusted friend who has a long credit history. The key is to make sure that they didn’t miss a payment or have any delinquencies. We can invest in tradelines a.k.a Credit piggybacking to help build your age of history. There are two types of credit piggybacking

- Traditional– Parent, Friend adds us as an authorized user.

- For-Profit– Pay to become an authorized user for a few months.

When you are added as an authorized user by a parent/friend the credit history will remain on your credit report. However, for the for-profit piggybacking, the history will be removed once the agreed time you selected is over and your score will return to where it was before the increase.

You can also invest in credit repair however there are some things you should know.

- You can repair your credit on your own

Surprise!!! Yes, you CAN indeed repair your credit on your own. There are tutorials in various forms that provide the strategies and sometimes even the templates that you can use to help guide you. Now, things do get a little complicated when there are legal issues reported on your credit file, but if you don’t have any legal issues like bankruptcy, tax liens, etc., then you can try to repair your credit yourself. If your efforts don’t work, and you still have inaccurate information being reported on your credit file, then consider a credit repair specialist.

- Yes, you still have to pay for your student loans

This is a common thing that a lot of people think about credit repair. Some believe that they will no longer have to pay for things like student loans if they get it removed from their credit report. That is not true. Make sure that you ask your credit repair specialist what accounts you still need to pay for if they end up being removed from your credit file. I can tell you upfront, student loans will be one of those things you still have to pay for even after it has been removed from your credit report.

- Credit repair is an investment

Credit Repair is not an overnight success story. When you begin your credit repair journey it will take some time for you to see results. Sometimes that may be 30-60 days or even 1-4 years. If you watched a credit repair video and saw someone getting their accounts removed in 2 weeks, you may not have the same experience. Just be patient and let the process play out. Now, I do understand that some credit repair companies charge a monthly fee to work on repairing your credit and that can be a bit frustrating if you’re not seeing the results you anticipated; however, remember, like I said, credit repair is an investment and takes time.

- 0ver 15 percent of those who got their credit repaired…wrecked their credit again and acquired some bad debt.

I was shocked when I saw this stat. This can happen in a few ways. Some people get their credit repaired and then use it to start various business ventures or apply for business credit and unfortunately get into deeper debt. Others continue the same credit borrowing habits that caused their initial negative credit accounts. I would advise two things. Please make sure that if you are new to starting a business and you’re not sure how to establish business credit properly, ask a professional first. Also, educate yourself on how to maintain good credit and practice good financial habits.

- There’s a possibility your credit won’t be “fully” repaired.

This will not be a selling point for a credit repair company, but these are things to keep in mind if you are considering credit repair. If your credit file has bankruptcies, tax liens, repossessions, and other severely negative items, these can be very tedious to remove, and the credit repair expert may not be able to remove all of your inaccurate information. In some cases, it’s because the creditor simply fixes their error and keeps reporting on the account, and in other cases, it’s due to the creditor having proof the account truly belongs to you.

Chapter 4

Different Types of credit cards

Secured credit card

A secured credit card is a card that requires the individual to put down a cash deposit for approval. Secured credit cards are great for those who are building credit or have poor credit. Please be sure to read the terms of use and understand that there may be fees associated with these cards. Some credit issuers have been known to have very unreasonable interest rates. *If you are unsure about a card or the fees associated with a secured card please reach out to a financial/credit expert.

Unsecured credit card

An unsecured credit card is a card that does not require collateral/ cash to be put down to be approved. These cards are mostly awarded lines of credit solely provided by the lender. Be sure to pay your balance monthly and not miss any payments. If you miss a payment it could result in a late payment fee as well as a late payment notice which is sent to the credit reporting bureaus and reports on your credit report, which could drop your credit score.

Charge credit card

A charge card is a type of credit card that allows the cardholder to charge purchases to their account and pay the balance in full each month. Charge cards typically have no pre-set spending limit, which can make them a good option for people who want the flexibility to spend as much as they need without having to worry about being approved for credit. charge cards also tend to have higher interest rates than other types of credit cards, so it’s important to make sure you can pay your balance in full each month before using one.

Store credit card

A store credit card is a credit card that can only be used at a specific retailer. Store credit cards often come with special benefits and rewards, such as discounts or points for every purchase made. Store credit cards can be a great way to save money on your favorite products or earn rewards while shopping. However, it is important to remember that store credit cards typically have higher interest rates than other types of credit cards, so it is important to pay off your balance in full each month. Store credit cards can be a great tool for budgeting and saving money, as long as you use them responsibly.

Business credit card

A Business credit card is a type of credit card specifically designed for businesses. Business credit cards offer a variety of benefits, including cash-back rewards, travel perks, and 0% APR periods. Business credit cards can help businesses manage their finances by providing a flexible line of credit that can be used for business expenses. Business credit cards also offer valuable insights into spending patterns and can help businesses track and manage their finances. Business credit cards are an essential tool for any business, small or large.

Invitation-only credit cards

Invitation-only credit cards are credit cards that are not available to the general public. They are usually offered by banks or other financial institutions to their best customers. Invitation-only credit cards often have better terms and conditions than regular credit cards, such as lower interest rates and annual fees. To get an invitation-only credit card, you usually need to have a good credit history and meet certain income requirements.

Student credit cards

Student credit cards are credit cards specifically designed for students. They typically have lower interest rates and credit limits than regular credit cards and may offer other perks such as cashback or rewards points. Student credit cards can help students build their credit history, which can be beneficial when they graduate and apply for jobs or loans.

Travel credit card

A Travel credit card is a type of credit card that offers perks and rewards specifically for travel expenses. These cards can offer a variety of benefits, such as earning points or miles that can be redeemed for free or discounted travel, priority boarding, and access to exclusive airport lounges. Travel credit cards also typically have no foreign transaction fees, which can save you money when making purchases in other countries.

Hotel credit cards

Hotel credit cards can be a great way to earn rewards on your hotel stays. They typically offer generous rewards programs and can even provide perks like free nights and upgrades. But before you apply for one of these cards, it’s important to understand how they work. Hotel credit cards usually come with an annual fee, but this fee is often offset by the rewards and perks you can earn. For example, some cards offer a free night at a hotel after you spend a certain amount of money on the card. Others may provide upgrades or discounts on your hotel stays.

Cash-back credit cards

Cashback credit cards are a great way to earn rewards on your everyday purchases. With most cash-back credit cards, you’ll earn a certain percentage back on all of your purchases, which can add up to big savings over time. Cash-back credit cards can be used for any type of purchase, so they’re a great way to earn rewards on everything from groceries to gas. And, best of all, many cash-back credit cards offer sign-up bonuses, so you can earn even more rewards in the first few months of using your card.

Balance Transfer Credit Card

With this type of card, you transfer the balance from another credit card with a higher interest rate to the balance transfer card, which usually has a much lower rate. This can help you save a lot of money in interest charges and can help you get out of debt more quickly.

What are the differences between business and personal credit files?

There are a few key differences between business and personal credit files. For businesses, credit files typically include information on the company’s financial history, payment history, and credit utilization. Personal credit files, on the other hand, generally only include information on the individual’s finances.

Another key difference is that businesses have “Dun & Bradstreet” scores, which are used to assess a company’s riskiness as a borrower, while personal credit scores are used to assess an individual’s riskiness as a borrower.

Finally, businesses can often get access to lines of credit that individuals cannot, such as business loans and lines of credit from suppliers. This is because businesses are considered to be less of a risk than individuals when it comes to borrowing money.

What is business credit?

Business credit is a type of credit that is specifically designed for business purposes. It can be used to finance business expenses, such as inventory or equipment purchases, and can also be used to help with business expansion. Business credit is typically offered by banks and other financial institutions.

There are several advantages to using business credit. First, it can help you manage your business finances more effectively. Second, it can give you access to financing that you may not be able to get through traditional channels. And third, business credit can help build your business’s credit history, which can be helpful down the road if you need to obtain additional financing.

If you’re thinking about using business credit, there are a few things to keep in mind. First, make sure you understand the terms and conditions of the credit agreement. Second, be sure to keep up with your payments, as business credit can impact your credit if you default on the loan. And finally, remember that business credit is a tool – use it wisely and it can help your business grow and thrive.

Chapter 5

No, No when building credit

Negative items can have a significant impact on your credit score. Depending on the item, it can stay on your report for up to seven years. This can make it difficult to get approved for loans or other lines of credit. negative items can also make it difficult to rent an apartment or get a job. If you’re trying to improve your credit score, it’s important to understand how negative items can affect it.

Here’s a short list:

- Late or missed payments

- Defaulting on a loan

- Applying for too many credit products in a short period

- Having a high credit utilization ratio

- Making frequent applications for credit

- Having a history of financial problems

- Having a low credit score

- Filing for bankruptcy

- Being the subject of a public record

- Engaging in excessive credit card use

- Late payments

Late payments can have a significant impact on your credit score. Payment history is one of the key factors that credit scoring models consider, so even one late payment can cause your score to drop. The effect of late payments on your credit score will depend on how late they are and how often you make them. Generally speaking, the more recent and frequent the late payments are, the more they will damage your score.

If you have late payments in your credit history, there are a few things you can do to help improve your credit score:

- Make all future payments on time: This will help show that you’re now reliable with your payments.

- Work with creditors to remove late payments from your credit report: This can be difficult, but if you’re able to get the late payments removed, it will improve your credit score.

- Use a credit monitoring service: This can help you keep track of your credit score and notify you if there are any changes.

- High balances

There are a few different ways that high credit card balances can affect your credit score. First, credit scoring models generally look at your credit utilization ratio, which is the amount of credit you’re using compared to the amount of credit you have available. If you have a high balance on one or more of your credit cards, it can increase your credit utilization ratio and lower your credit score.

Also, high credit card balances can indicate to lenders that you’re struggling to manage your debt. This can make it difficult to get approved for new credit products and can lead to higher interest rates if you are approved.

- Too many Inquiries

Too many credit inquiries can hurt your credit score. Each time you apply for credit, lenders will check your credit report and this will be recorded as an inquiry. If you have too many inquiries on your credit report, it can signal to lenders that you are a high-risk borrower and make it more difficult for you to get credit in the future.

Inquiries can also stay on your credit report for up to two years and can have a small, negative impact on your credit score. So if you’re planning on applying for credit shortly, it’s important to be mindful of how many inquiries you have.

- Defaults

When you default on a loan, it can have a major impact on your credit score. Defaulting means that you have failed to make payments on your loan as agreed, and this can lead to negative marks on your credit report. This can in turn lower your credit score, making it more difficult to get approved for new loans or credit lines in the future. Additionally, a default can stay on your credit report for up to seven years, making it one of the most damaging credit history items you can have. If you’re struggling to make payments on a loan, it’s important to contact your lender as soon as possible to discuss your options.

- Charge-offs

Charge-offs can have a significant impact on our credit score. A charge-off is when a lender decides that we have defaulted on a debt and they write it off as a loss. This information will then stay on our credit report for up to seven years, which can make it difficult to get approved for new credit during that time. Charge-offs can also make it difficult to get approved for a loan or credit card with a good interest rate. If you have a charge-off on your credit report, it’s important to try to negotiate with the lender to have it removed. You can also dispute the charge-off with the credit bureau if you believe it is inaccurate.

- Collections

If you have a collection on your credit report, it can negatively impact your credit score. This is because collection accounts are considered to be high-risk by credit scoring models. Collections can stay on your credit report for up to seven years and will therefore lower your credit score for the duration of that time.

- Foreclosures

Foreclosures can have a significant impact on your credit score. If you’re behind on your mortgage payments and facing foreclosure, your credit score will take a hit. The further behind you are, the more your score will suffer. A foreclosure will stay on your credit report for seven years and can make it difficult to get approved for credit during that time. If you’re able to avoid foreclosure, you can help reduce the damage to your credit score. If you’re already in foreclosure, there are still things you can do to minimize the impact on your credit score. You can try to negotiate with your lender to have the foreclosure removed from your credit report if you catch up.

- Repossessions

A repossession is when a lender takes back possession of an asset, such as a car, that you have failed to make payments on. This can happen after a foreclosure or if you simply stop making your car payments. A repossession will stay on your credit report for seven years and can have a major impact on your credit score. Your credit score can drop by 100 points or more after a repossession. This can make it very difficult to get a loan or qualify for a mortgage.

- Bankruptcies

Bankruptcies can have a significant impact on your credit score. Depending on the type of bankruptcy, it can stay on your credit report for up to 10 years. This can make it difficult to get credit in the future. There are two common types of bankruptcies that can be filed for an individual: Chapter 7 and Chapter 13. Chapter 7 bankruptcy stays on your credit report for up to 10 years and can significantly lower your credit score. Chapter 13 bankruptcy stays on your credit report for up to 7 years and can also lower your credit score, but not as much as Chapter 7.

- Liens

Liens can have a significant impact on your credit score. A lien is a legal claim against your property, and it can be placed by creditors, the government, or other entities. If you have a lien on your property, it means that the entity who placed the lien has a right to take possession of your property if you don’t pay what you owe. Liens can stay on your credit report for up to seven years, and they can have a major negative impact on your credit score. If you’re trying to improve your credit score, it’s important to understand how liens can affect your credit.

What happens if I don’t pay the debt, I owe on my credit card?

If you don’t pay the debt you owe on your credit card, late fees, and interest will begin to accrue. If you continue to miss payments, your account may be frozen or closed, and your credit score will suffer. In extreme cases, your debt may be “charged off,” which means the creditor has given up on trying to collect it and has written it off as a loss. This will damage your credit score even further.

More No No’s when building credit

- Not looking at your credit report

Many people don’t realize that not looking at their credit report can hurt their credit score. By not monitoring your credit report, you could miss important information that could help you improve your credit score. Additionally, if there are any inaccurate items on your credit report, you may not be aware of them, and they could continue to negatively impact your credit score. So, it’s important to review your credit report regularly to ensure accuracy and to identify any potential areas for improvement.

- Not reading the fine print

Not reading the fine print can have several consequences, some of which may be serious. For example, if you’re signing up for a credit card, not reading the fine print could mean that you miss important information about interest rates or fees. This could end up costing you a lot of money in the long run. Additionally, not reading the fine print on contracts or other legal documents can result in misunderstanding your rights and obligations, which could lead to problems down the road. In short, it’s always best to read the fine print carefully before agreeing.

- Exceeding your credit limit

If you exceed your credit limit, it can hurt your credit report. Lenders will see this as a sign that you’re struggling to manage your finances, which could make it harder for you to get approved for credit in the future. Additionally, exceeding your credit limit can lead to fees and higher interest rates. Therefore, it’s important to keep an eye on your credit limit and try to avoid going over it. If you do end up exceeding your credit limit, be sure to contact your lender right away and explain the situation. They may be willing to work with you to help avoid any negative consequences.

- Applying for every card you get an invitation for

When you are trying to improve your credit score, it is important to be mindful of the impact that each credit card application can have. Applying for too many credit cards at once can hurt your credit score, as it signals to lenders that you may be in financial distress. Additionally, each credit inquiry will stay on your credit report for two years, so it’s best to space out your applications to avoid damaging your credit score.

- Max out your credit cards

Maxing out your credit cards can hurt your credit report. This is because credit utilization, which is the amount of credit you’re using compared to your credit limit, is one of the factors that are used to calculate your credit score. If you have a high credit utilization, it can indicate to lenders that you’re struggling to manage your debt, which can make it harder to get approved for new credit. Additionally, maxing out your credit cards can lead to higher interest rates and fees if you’re unable to pay off your balance in full each month.

Chapter 6

How to apply for credit? How can we leverage our good credit?

If you are new to building credit, please research cards that are for those who are looking to build credit. It will be difficult to apply for top-tier cards if you don’t have a credit history. When you’re first starting you might consider starting with a secured credit card. A secured credit card is a card that requires the individual to put down a cash deposit for approval. Secured credit cards are great for those who are building credit or have poor credit. Please be sure to read the terms of use and understand that there may be fees associated with these cards. Before you apply do more research there may be unsecured cards (No collateral needed) for you to start building credit.

If you’re new to credit, you might be wondering how to apply for a credit card. Here’s a quick overview of the process:

- Check your credit score

Before you apply for a credit card, it’s a good idea to check your credit score to see where you stand. This will give you an idea of which cards you may be eligible for. You can check your credit score for free on sites like Credit Karma or Bankrate.

- Research credit cards

Once you know your credit score, start researching credit cards that are right for you. Look for cards with features that fit your needs, such as low-interest rates, rewards programs, and no annual fees.

- Compare offers

Once you’ve narrowed down your options, it’s time to compare credit card offers. Make sure to read the fine print so you understand all the terms and conditions of each card.

- Apply for the card online

Make sure you’re in a secure browser! After you finish the application, you will get a response in 30 seconds or your application will be reviewed and you will get a decision by mail or email.

For those who have some credit history and are looking to build credit here are some tips when you apply for credit.

Make sure your finances are in shape

One of the first things that lenders will look at when you apply for credit is your financial history. They want to see how well you’ve managed your money in the past, and whether or not you’re likely to repay any credit they extend to you.

If you have a history of missed payments, maxed-out credit cards, or other financial problems, it’s going to be difficult to get approved for a new credit card. On the other hand, if you have a good track record of managing your finances responsibly, you’re more likely to be approved. That’s why it’s so important to make sure your finances are in good shape before you apply for credit. Take some time to review your credit report, make sure there are no errors and try to improve your credit score if it’s not as high as you’d like. Then, when you do apply for a credit card, you’ll have a better chance of being approved.

Do not apply for multiple cards in one day

When you apply for credit cards, the credit card issuer will usually do a hard pull on your credit report. This can lower your credit score and make it harder to get approved for other credit products. Additionally, applying for multiple credit cards in a short period can look like you’re desperate for credit, which can also negatively impact your chances of getting approved. So, if you’re planning on applying for multiple credit cards, it’s best to space out your applications over a period of weeks or months.

Don’t lie about your income

It’s important to be honest when you’re applying for credit. Lying about your income could lead to being approved for a credit card that you can’t afford, which could put you in financial jeopardy. Additionally, if you’re caught lying on a credit application, you could be subject to penalties or legal action. So, it’s simply not worth it to take the risk – be honest on your credit applications and you’ll be in much better shape financially. Sometimes the lender will ask for your w-2 before they approve you for the card you’re asking for.

The credit application process is similar

- Find the right credit card for you. There are dozens of different credit cards out there, so make sure you do your research and find one that best suits your needs.

- Once you’ve found the right credit card, head to the issuer’s website and begin the application process. You’ll typically be asked to provide some basic information about yourself, as well as your financial history.

- Once you’ve submitted your application, it will undergo a review process. If everything looks good, you should receive an approval within a few minutes.

- Once you’re approved, you’ll need to activate your credit card and start using it. Make sure you keep track of your spending and make timely payments, as this will help you build a good credit history.

Perks of having excellent credit

- You may be able to get a lower interest rate on a loan.

- Excellent credit can help you get approved for a loan with more favorable terms and conditions.

- Excellent credit can give you more negotiating power when it comes to the interest rate and other terms of your loan.

- Excellent credit may allow you to avoid paying certain fees, such as origination or prepayment penalties.

- Excellent credit can help you qualify for special financing programs that offer lower interest rates or other benefits.

- Excellent credit can make it easier to rent an apartment or obtain utility services.

- Excellent credit can help you get a job or obtain insurance at a lower rate.

- Excellent credit can help you qualify for a rewards credit card with valuable perks.

- Excellent credit can make it easier to borrow money in the future if needed.

- Excellent credit is a valuable asset that can help you reach your financial goals.

How can I leverage good credit?

Real Estate Investing: If you have very good or excellent credit, you may be able to leverage that to get a better deal on real estate. For example, you may be able to negotiate a lower interest rate or down payment. Having good credit can also help you get approved for financing more easily. We can use the opportunity depending on market conditions to buy multifamily properties. Or make some renovations around the house that can increase the value of the home. By using leverage, you can access more money to invest in assets that can appreciate over time. This can help you boost your returns and grow your wealth faster than if you were only using your savings.

Of course, it’s important to be smart about how you use leverage. Taking on too much debt can be a risky proposition, so it’s important to make sure you understand the risks involved before taking out any loans. But used wisely, leverage can be a powerful tool for building wealth.

Better insurance rates

If you have very good or excellent credit, you may be able to leverage that to get better insurance rates. Insurance companies often take credit scores into account when determining rates, so having a strong score could save you money on your premiums.

There are a few ways to go about this. You can shop around and compare rates from different insurers, or you can talk to your current insurer about what discounts they offer for good credit. Either way, it’s worth exploring your options to see if you can get a better deal on your insurance by leveraging your strong credit score.

Rare in these markets but they do exist. 0% intro APR auto loan

Get a 0% intro APR auto loan: If you have excellent credit, you may be able to get a 0% intro APR auto loan. This means you can finance your car and make monthly payments without paying any interest for a certain period (usually 12-24 months). This can be a great way to save on interest if you need to purchase a new car.

Chapter 7

How to deal with collections and student loan debt?

I remember getting a call from a collector years ago. I was a student in college and didn’t have the money to pay for the debt owed. The collector left a message and mentioned taking legal action if I don’t call back in the next 48 hours. I was really scared and after class, I wondered if they would show up at my apartment or if I would be served.

If you’re dealing with collection agencies, there are a few things you should keep in mind. First of all, collection agencies are trying to collect a debt that you owe. They’re not going to be your friend or try to help you out. They’re just trying to get the money that you owe. Second, collection agencies are regulated by the government. This means that they have to follow certain rules and regulations. You can find out more about these by contacting your state’s attorney general’s office or the Federal Trade Commission. Third, collection agencies may use tactics that seem unfair or harassing. However, they are allowed to do this as long as they don’t break the law. If you think that a collection agency is breaking the law, you can file a complaint with the FTC or your state’s attorney general’s office.

Here are some things we can do when dealing with collection agencies

- Get the Agencies information

If you’re being called by a collection agency, there are a few things you can do to get information from them. First, ask for the name and address of the collection agency. This will help you determine if they are legitimate. Next, ask for the amount of the debt and the reason for the call. Finally, ask if they are willing to provide written documentation of the debt. If they are not willing to provide this information, you may want to consider speaking with an attorney.

- Demand that you get everything in writing

If you’re dealing with collection agencies, it’s important to demand that everything be in writing. This way, you can keep track of what’s being said and avoid any misunderstandings. Collection agencies are required by law to send you a written notice within five days of first contacting you. This notice must include the amount of the debt, the name of the creditor, and your rights under the Fair Debt Collection Practices Act.

If the collection agency does not send you this notice, or if they make any false or misleading statements in it, you can file a complaint with the Consumer Financial Protection Bureau. The collection agency will also have to provide you with an itemized statement of the debt if you request it in writing. This statement must include the amount of the debt, the name of the creditor, and a breakdown of any interest and fees.

- Examine the bill the agency sends you

- Check the date of the bill. The collection agency should only be billing you for debts that are less than 180 days old. If the debt is older than that, the collection agency can’t legally collect it.

- Make sure the collection agency has included all required information on the bill, including your name, address, and account number.

- Verify that the collection agency is only charging allowed fees. Collection agencies are allowed to charge a maximum of $30 in collection fees, plus any interest that may be due on the debt.

- Check the math on the bill to make sure there are no errors.

- If you have any questions about the bill, contact the collection agency and ask for clarification. Don’t just assume that everything on the bill is accurate. collection agencies are known for making mistakes, so it’s always best to double-check.

- Educate yourself on the law for collection agencies

There are several ways to educate yourself on the law when it comes to collection agencies. One way is to speak with an attorney who specializes in this area of law. Another way is to research the laws and regulations online or at your local library. Additionally, you can attend seminars or workshops offered by collection agencies or other organizations that focus on this topic. Finally, you can always contact your state’s consumer protection agency for more information and resources.

- Request a debt validation

- Contact the collection agency in writing and request debt validation. Be sure to include your account number and collection agency contact information.

- The collection agency has 30 days to respond. If they don’t, the debt is considered invalidated.

- Once you receive the validation, review it carefully. Make sure it includes the original creditor’s information, the date of the last payment, and the amount owed. If anything looks incorrect, dispute it with the collection agency.

- If you still believe you owe the debt, you can negotiate a payment plan with the collection agency. If you’re able to agree, be sure to get it in writing before making any payments.

- Check to see if the debt is past its statute of limitation

The statute of limitations on debt varies from state to state but is typically between three and six years. This means that after a certain amount of time has passed, the collection agency can no longer take legal action against you to collect the debt.

Of course, this doesn’t mean that the debt disappears. The collection agency may still contact you and try to convince you to pay, but they can’t take any legal action against you.

If you think a collection agency is trying to collect on a debt that’s past the statute of limitations, you can send them a “cease and desist” letter telling them to stop contacting you. You can find template letters online.

- Avoid giving personal information

There are a few things to keep in mind when it comes to avoiding giving out personal information. First, be aware of collection agencies. These organizations may contact you and request personal information to collect on a debt. If you do not have a legitimate debt with the collection agency, do not provide any personal information.

Also, be cautious of any unsolicited requests for personal information. This can come in the form of an email, text message, or phone call. If you did not initiate the contact, be wary of giving out any information.

How to deal with student loan debt

The president has forgiven $10,000 of student loan debt for borrowers that are making under $125,000 a year. For millions of Americans, this didn’t even put a dent in their student loans. Here are some things we can do to pay down our student loan debt.

- Budget

One of the first steps we can take to pay down our student loans is to create a budget. First, we must determine how much money we have coming in each month and what our regular expenses are. We can create an excel sheet, use an app, or just simply use pen and paper. Some bank apps show us how much of our money is being allocated to specific areas. This can help us to quickly identify our expenses. After we’ve created our list, we can see where we can cut back to put more money towards our student loans.

- Consolidate your loans

If you have multiple student loans, it may be helpful to consolidate them into one loan. This can make it simpler to manage your payments and may even get you a lower interest rate. A lower interest rate can help us save money over the life of your loan and help us pay it down faster. Another option that we have when we consolidate our loans is to extend our repayment term. Extending our repayment term will make our payments more affordable however…the interest rate will most likely be high. Please be sure to speak with the student loan provider to figure out if consolidating your loans is right for you.

- Get a part-time job

Working a part-time job can help pay down the amount of debt you have. Even if you only make a few hundred dollars each month, that can add up over time and make a big difference. You can use the money from the part-time job to apply to the principal of our loan to knock down the balance.

- Look into student loan forgiveness programs

The Public Service Loan Forgiveness Program. This program forgives student loans for those who work in public service. To qualify, you must make 120 monthly payments while working full-time for an eligible employer. The Income-Based Repayment Plan. This plan allows you to make lower monthly payments based on your income. If you make payments for 20 or 25 years, depending on when you took out your loan, the remaining balance may be forgiven.

A myth about student loans

If my student loans are not on my credit report, I don’t have to pay

This is not true. If you owe money on your student loan amount. You need to continue to pay the amount owed each month. The student loans not reporting to your credit report is good news, because it will not affect your debt-to-credit ratio.

If I file for bankruptcy my student loans will go away.

It’s important to note that this does not mean that your student loan debt is gone forever. You will still owe the money, and the lender can continue to try to collect it from you after your bankruptcy case is closed. However, filing for bankruptcy can give you some much-needed breathing room when it comes to student loan debt. Student loans can not be discharged in a bankruptcy

Consolidating your loans will make them more expensive

Consolidating your student loans can be a good way to save money on interest and simplify your monthly payments. However, there are some situations where consolidating your student loans may not be the best option. For example, if you have the opportunity to get a low-interest student loan, it may be worth taking out the loan and using the money to pay off high-interest debt, such as credit card debt.

Chapter 8

How to protect yourself from identity theft

One of the best ways to protect yourself from identity theft is to regularly check your credit report. You can get a free credit report from each of the three major credit bureaus once per year. This will help you spot any suspicious activity on your account.

Another way to protect yourself is to be careful about whom you give your personal information to. Be wary of anyone who asks for your Social Security number or other sensitive information without a good reason. Only provide this information when you are sure it is safe to do so.

You should also keep an eye on your bank and credit card statements for any unauthorized charges. If you see anything suspicious, report it to your financial institution right away.

Identity theft can be a major hassle, but it is important to remember that you can take steps to protect yourself. By staying informed and being cautious with your personal information, you can help reduce your risk of becoming a victim. credit report, credit bureau, credit card statement, Social Security number, bank statement, identity theft, and personal information.

- Check your credit report regularly.

It’s important to keep an eye on your credit report to make sure that everything is in order and to avoid identity theft. Here are some tips on how to check your credit report regularly:

- Review your credit report at least once a year. You can get a free copy of your credit report from each of the three major credit bureaus (Experian, TransUnion, and Equifax) once every 12 months at AnnualCreditReport.com.

- Check for any discrepancies. If you see anything on your credit reports that doesn’t look right, such as an account that you don’t recognize or a late payment that you don’t remember making, contact the credit bureau immediately.

- Be proactive about monitoring your credit. In addition to checking your credit report periodically, you can also sign up for a credit monitoring service, which will alert you if there are any changes to your credit report.

- Be vigilant about credit card activity.

It’s important to be vigilant about credit card activity to avoid identity theft. One of the top things we can do to protect ourselves from identity theft is to leave our saved information on our computers. Delete credit card information and personal information from the auto-fill. Here are some additional tips:

- Check your statements regularly. If you see anything suspicious, report it to your bank immediately.

- Keep an eye on your credit score. If it suddenly drops, this could be a sign that someone has stolen your identity and is using your information to open new accounts.

- Be careful about whom you give your information to. Only provide it to trusted websites and businesses.

- Shred any documents that contain your personal information before disposing of them.

- Keep your Social Security number safe.

It’s important to take steps to protect your Social Security number (SSN) to avoid becoming a victim.

There are a few simple things you can do to keep your SSN safe from identity thieves:

- Keep your SSN card in a secure place, such as a locked box or drawer. Don’t carry it with you unless necessary.

- Don’t give out your SSN to anyone unless you are sure they need it and you trust them. Be especially careful about giving out your SSN online.

- Shred any documents that contain your SSN before throwing them away. This includes old tax returns, bank statements, and credit card offers.

- Protect your computer by using security software and creating strong passwords. This will help protect your personal information if your computer is lost or stolen.

- Protect your computer from malware and viruses.

One way that identity thieves can get your information is by installing malware on your computer. Malware is software that is designed to harm your computer or steal your personal information. Once installed, malware can do several things, including logging keystrokes, stealing passwords, and accessing personal information.

Another way that identity thieves can get your information is by phishing. Phishing is when someone sends you an email or text message that looks like it comes from a legitimate source but is a scam. The message will often try to trick you into clicking on a link or opening an attachment that contains malware.

To protect yourself from identity theft, it is important to keep your computer safe from malware. Use a reputable antivirus program and keep it up to date. Be careful about what you click on, and only open emails and attachments from people you know. If you think you may have been a victim of identity theft, contact your local law enforcement agency.

- Avoid phishing scams.

Phishing is when someone tries to trick you into giving them your personal information, usually by sending you an email or pop-up message that looks like it’s from a legitimate company or website. They might say there’s a problem with your account or offer a prize or discount if you click on a link. But if you do, you’ll be taken to a fake website where you’re asked to enter sensitive information like your Social Security number, credit card number, or bank account information.

If you give out this information, identity thieves can use it to open new accounts in your name, make unauthorized charges on your existing accounts, or even get a job or file for benefits using your identity.

That’s why it’s important to be aware of phishing scams and know how to protect yourself from them. Here are some tips:

- Be suspicious of any email or pop-up message that asks for personal or financial information. Even if the message looks like it’s from a company you know, don’t reply or click on any links unless you’re sure it’s legitimate.

- If you’re not sure whether an email is real, contact the company directly. Don’t use the contact information in the email; instead, find the company’s website and look for their customer service number or email address.

- Keep your antivirus and anti-spyware software up to date and run regular scans of your computer. This will help protect you from malware that can be used to steal your personal information.

- Be cautious about giving out personal information on the phone, even if the caller seems to have some of your basic information like your Social Security number or address. identity thieves may use this tactic to try to get more information from you. If you’re not sure who’s calling, hang up and call the company back using a number you know is real.

- Keep an eye on your bank and credit card statements.

Review your statements regularly. Ideally, you should check them at least once a month.

- Compare your statements to your records. Make sure that all of the charges on the statement are ones that you’ve made.

- Watch out for unauthorized transactions. If you see any charges that you don’t recognize, report them to your bank or credit card company right away.

- Keep an eye on your account balance. If it suddenly decreases, it could be a sign that someone has stolen your information and is using your account.

Chapter 9

Credit Laws and Consumer Rights Protection

Credit Laws are designed to protect consumers from unfair or deceptive practices by businesses that extend credit. Credit laws also establish standards for how businesses must disclose information about credit terms and conditions. The federal government enforces credit laws through the Consumer Financial Protection Bureau, which is responsible for implementing and enforcing federal consumer financial laws.

Credit Laws cover a wide range of topics, including credit reporting, debt collection, and bankruptcy. Credit reporting laws help ensure that consumers have access to accurate information about their credit history. Debt collection laws protect consumers from abusive debt collection practices. And bankruptcy laws provide consumers with a way to get relief from unmanageable debt.

There are several laws in place that protect consumers from unfair or deceptive practices by businesses. These laws are designed to ensure that businesses treat customers fairly and transparently and to give customers the information they need to make informed decisions about products and services.

The main law governing consumer rights is the Consumer Rights Act 2015, which consolidates several previous statutes into one piece of legislation. The Act sets out several rights that consumers have when dealing with businesses, including the right to:

The Consumer Bill of Rights includes the following rights:

- The right to be informed about your rights as a consumer

- The right to fair treatment by businesses

- The right to choose which products or services to buy

- The right to safety about products and services

- The right to be heard when you have a complaint about a product or service

- The right to redress if you have been treated unfairly by a business.

In addition to the Consumer Rights Act, several other laws offer protection to consumers. These include the Sale of Goods Act 1979, which gives consumers certain rights when buying goods from businesses, and the Unfair Contract Terms Act 1977, which protects consumers from unfair terms in contracts.

If you feel that you have been treated unfairly by a business or given misleading information, you can make a complaint to your local Trading Standards office. Trading Standards officers will investigate your complaint and take action against the business if they find that it has breached consumer law.

Headquarters

Federal Trade Commission

600 Pennsylvania Avenue, NW

Washington, DC 20580

Telephone: (202) 326-2222

Constitution Center

Federal Trade Commission

400 7th St., SW

Washington, DC 20024

Telephone: (202) 326-2222

NOTE: Send mail only to 600 Pennsylvania Ave., NW (Headquarters) address above.

For Consumers

Report fraud, scams, and bad business practices at ReportFraud.ftc.gov.

Report identity theft at IdentityTheft.gov.

Report unwanted calls at donotcall.gov.

Chapter 10

Credit Definitions

Annual Percentage Rate (APR): The APR is the annual cost of borrowing money, including interest charges and any other fees associated with the loan.

Balance: The balance is the outstanding amount owed on a loan or line of credit.

Credit Score: A credit score is a numerical representation of your creditworthiness, based on information in your credit report.

Credit Report: A credit report is a detailed record of your credit history, including information on your payment history, outstanding debt, and credit inquiries.

Credit Limit: A credit limit is a maximum amount you’re allowed to borrow on a loan or line of credit.

Debt-to-Income Ratio (DTI): Your DTI is a measure of how much debt you have relative to your income. Lenders use this ratio to determine your ability to repay a loan or line of credit.

Fixed-Rate Loan: A fixed-rate loan has an interest rate that stays the same for the life of the loan.

Variable-Rate Loan: A variable-rate loan has an interest rate that can change over time, typically in response to changes in the prime rate.

Grace Period: A grace period is a time between when a bill is due and when late fees begin accruing.

Interest Rate: The interest rate is the cost of borrowing money, expressed as a percentage of the loan amount.

Late Fee: A late fee is a charge assessed by a lender for making a payment after the due date.

Minimum Payment: The minimum payment is the smallest amount you’re required to pay on your loan or credit card each month.

Origination Fee: An origination fee is a charge assessed by a lender for processing a loan or line of credit.

Over-the-Limit Fee: An over-the-limit fee is a charge assessed by a lender for exceeding your credit limit.

Prepayment Penalty: A prepayment penalty is a fee charged by some lenders if you pay off your loan or line of credit early.

Principal: The principal is the amount of money borrowed on a loan, not including interest or any other fees.

Secured Loan: A secured loan is a loan that’s backed by collateral, such as a car or home equity.

Unsecured Loan: An unsecured loan is a loan that’s not backed by collateral.

Statement Balance: The statement balance is the amount owed on a loan or credit card as of the statement date.

Term: The term is the length of time you have to repay a loan.

Origination Date: The origination date is the date on which a loan or line of credit was issued.

Statement Date: The statement date is the date on which a lender states a loan or line of credit.

Minimum Monthly Payment Due: The minimum monthly payment due is the smallest amount you’re required to pay each month on your loan or line of credit.

Closing Date: The closing date is the date on which a loan or line of credit is closed and no longer active.

Fixed Rate: A fixed rate is an interest rate that doesn’t change over time.

Variable Rate: A variable rate is an interest rate that can change over time, typically in response to changes in the prime rate.

Annual Fee: An annual fee is a charge assessed by a lender for maintaining a loan or line of credit over the course of a year.

Cash Advance Fee: A cash advance fee is a charge assessed by a lender for taking out a cash advance on your loan or line of credit.

Late Payment Fee: A late payment fee is a charge assessed by a lender for making a payment after the due date.

Returned Payment Fee: A returned payment fee is a charge assessed by a lender for a payment that’s returned due to insufficient funds.